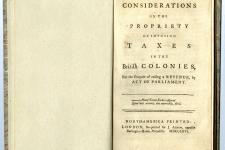

African taxation system remains unfair since colonial times

Taxation remains the primary source for funding public goods, like healthcare, education, infrastructure, and maintaining law and order. This chapter shows that while equity and fairness principles are fundamental in a good tax system, during colonial times, these were violated to suit the logic of the unjust colonial system. The most profitable tax base, the extractive sectors such as mining, remained largely untaxed or undertaxed. The colonial tax system was dual, burdening Africans with both “native” (e.g., hut taxes which were levied on every African dwelling, which were mostly huts) and “modern” taxes (direct and indirect taxes). In contrast, colonial settlers paid proportionately lower modern taxes since they were responsible for setting the tax rules.

Postcolonial taxation systems maintain this dual structure, although one with a different logic to the colonial system. Elites and high-net-worth individuals either influence tax rules or can neglect them. This undermines fairness: those who should contribute more pay very little or nothing, at times in cahoots with foreign companies that can take advantage of globalisation and lapses in the international tax systems. The most lucrative African tax base (mainly the extractive sector) remains untaxed or undertaxed. Consequently, mobilised tax revenues are very low, jeopardising progress on sustainable development goals and climate action. The international community, including foreign companies and countries, played a role during the colonial extractive-low tax systems and in a different setting, this continues to happen now. Raising more revenues requires a fairer tax system, and for this, both the domestic and international players are relevant.

DIIS Experts